What Is the Endowment Model — and Why Does It Matter for Your Portfolio?

The investment approach behind some of the world's most resilient portfolios, and how we use its principles to build wealth for our clients.

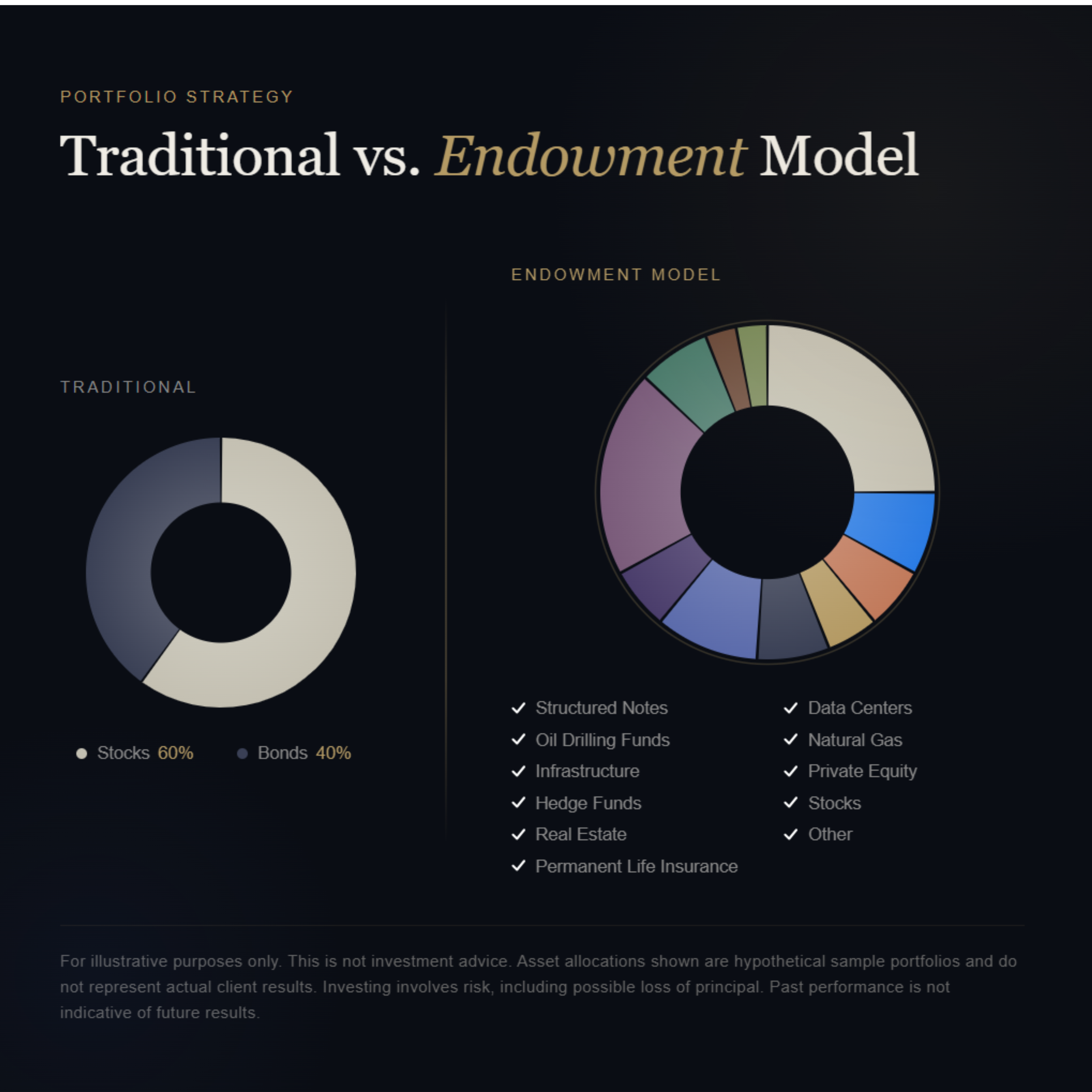

When most people think about investing, they picture two things: stocks and bonds. Maybe a mutual fund. Perhaps an index ETF. This is the world of the traditional 60/40 portfolio — 60% equities, 40% fixed income — and for decades, this has been the default approach for most retail investors and their financial advisors alike.

It's not a bad strategy. But it's also not the only one. And for the institutions that manage some of the largest, most sophisticated pools of wealth in the world — university endowments, foundations, sovereign wealth funds — a 60/40 portfolio would be considered almost quaint.

Those institutions use a different framework. It's commonly called the Endowment Model. And understanding it is central to understanding how we think about building portfolios at Axiom Wealth.

WHERE DID THE ENDOWMENT MODEL COME FROM?

The story starts at Yale University in the 1980s, when David Swensen took over as Chief Investment Officer with a mandate to do something radical: stop investing like everyone else.

At the time, Yale's endowment — like most institutional portfolios — was heavily concentrated in domestic stocks and bonds. Swensen believed this was leaving significant value on the table. His thesis was straightforward: markets reward investors who are willing to accept illiquidity, complexity, and unconventional asset classes that most investors either can't access or aren't willing to hold.

Over the next few decades, Swensen transformed Yale's endowment into one of the most successful institutional investment programs in history, generating annualized returns that consistently outpaced traditional benchmarks. The core insight wasn't just about picking better stocks. It was about thinking completely differently about what a portfolio could contain.

“The Endowment Model isn’t a product. It’s a philosophy — one built on diversification that actually means something.”

Harvard, Princeton, Stanford, and other major endowments followed suit. Today, the Endowment Model — sometimes called the Yale Model — is recognized as one of the most influential frameworks in institutional investing.

WHAT MAKES IT DIFFERENT FROM A TRADITIONAL PORTFOLIO

The fundamental difference is the breadth of asset classes involved. A traditional 60/40 portfolio draws from two buckets. The Endowment Model draws from many — including categories that have historically been unavailable to everyday investors.

The key word here is correlation. When stocks fall sharply, bonds sometimes provide a buffer — but not always, and not always enough. 2022 is the most recent example of this. The Endowment Model seeks assets that behave differently from one another, so that a downturn in one area doesn't drag down the entire portfolio.

WHAT TYPES OF ASSETS DOES THIS PHILOSOPHY DRAW FROM?

The asset classes associated with endowment-style investing are varied, and not all of them are appropriate for every investor. But understanding the landscape is useful. Here are some of the categories most commonly associated with this approach:

Private Equity — Ownership stakes in private companies, often delivering higher long-term returns in exchange for illiquidity.

Infrastructure — Assets like energy pipelines, data centers, and utilities — stable cash flows with low market correlation.

Natural Resources — Commodities and energy assets including natural gas and oil, providing inflation protection and diversification.

Hedge Funds — Strategies designed to generate returns in both rising and falling markets through sophisticated hedging.

Structured Notes — Customized instruments with defined return profiles, often providing downside protection with market participation.

Permanent Life Insurance — Tax-advantaged vehicles that serve both protection and wealth accumulation purposes within a broader plan.

Public Equities — Traditional stocks still have a role — but as one component among many, not the entire portfolio.

THIS ISN'T A RIGID FORMULA — IT'S A WAY OF THINKING

One of the most important things to understand about the Endowment Model is that it isn't a specific product or a prescribed set of allocations. There's no single correct version of it. Yale's endowment looks different from Harvard's. A family office in Dallas applies it differently than a pension fund in California.

What they share is a mindset: a commitment to genuine diversification across asset classes, a willingness to look beyond public markets, and a focus on long-term compounding rather than chasing short-term performance.

At Axiom Wealth, we use the principles of the Endowment Model as a framework — not a template. Every client's situation is different. Age, income, tax circumstances, liquidity needs, and risk tolerance all shape how these principles get applied. What we're borrowing from the endowment playbook is the philosophy: that a well-constructed portfolio should look broader, more resilient, and more thoughtfully assembled than a simple split between stocks and bonds.

WHY DOES THIS MATTER NOW?

The 60/40 portfolio had a rough few years. In 2022, both stocks and bonds fell simultaneously — an event that wasn't supposed to happen, according to the conventional wisdom underlying that approach. Investors who had been told they were "diversified" found out they weren't, at least not in the way they had assumed.

Meanwhile, the landscape for individual investors has genuinely opened up. Alternative asset classes and private market strategies that were once reserved for institutional investors are increasingly accessible. The tools that endowments have used for decades are no longer out of reach.

That doesn't mean everyone should rush into alternatives or abandon traditional investments entirely. It means the conversation has expanded. And for investors who are serious about growing and protecting long-term wealth, that expanded toolkit is worth understanding.

WHAT THIS LOOKS LIKE IN PRACTICE

When we sit down with a new client, we're not handing them a pre-built product. We're having a conversation about what they actually need their money to do — when they need access to it, what they're trying to protect, and where they have flexibility to accept a different kind of risk in exchange for a different kind of return.

From there, we look across the full range of available tools and strategies. Some clients' portfolios will include structured notes alongside traditional equities. Others might benefit from exposure to private equity or real assets. In some cases, permanent life insurance plays an important role in the overall wealth picture. The right mix depends entirely on the individual.

What doesn't change is the underlying philosophy: build something that's genuinely diversified, that can weather different market environments, and that gives your wealth the best chance of compounding over time — the way endowments have done for generations.

If you're curious about how endowment-style thinking applies to your own financial situation, we'd love to start the conversation. No pressure — just a straightforward look at where you are and where you want to go.

DISCLAIMER: For informational and educational purposes only. This is not investment advice. All investing involves risk, including possible loss of principal. Alternative investments may involve additional risks including illiquidity, complexity, and limited regulatory oversight. Asset allocation and diversification do not guarantee a profit or protect against loss. Past performance is not indicative of future results. Please consult with a qualified financial professional regarding your specific situation before making any investment decisions.